How Risky Are Property Funds and REITs with Debt During COVID-19?

The outbreak of COVID-19 has caused many businesses to lose revenue for a period due to government regulations during the curfew aimed at controlling the spread of the virus, such as the closure of shopping malls, conference and exhibition venues, cinemas, and hotels in certain areas like Hua Hin and Phuket during the curfew. However, the situation in Thailand has improved, and the spread of the virus is now relatively well controlled. In contrast, the pandemic continues abroad, which poses a risk of a second wave in Thailand from incoming travelers. Due to this risk, Thailand cannot let its guard down and must enforce a quarantine (State Quarantine) for 14 days, resulting in a lack of foreign tourists entering the country.

Under such circumstances, many businesses are facing liquidity issues, and if they borrow money, it will affect their ability to repay debts. The Bank of Thailand has provided assistance to debtors affected by COVID-19 through various relief measures, including postponing principal and interest payments for over 15.11 million borrowers, amounting to debts worth over 700 billion baht. However, the debt relief measures are limited to a period of 3 – 12 months, depending on the case. Once this grace period ends, businesses will immediately face debt obligations again and may have to shut down permanently if the economy does not recover, unless they receive additional support.

At this point, readers may wonder whether Property Funds and REITs will be affected by debt issues. Is there a risk of liquidity shortages, or will they be unable to pay dividends? Funds investing in real estate such as hotels, conference and exhibition venues, airports, and shopping malls are likely to be significantly impacted by the COVID-19 situation compared to office buildings, factories, and warehouses, making them more vulnerable if they have higher debt obligations. The key debts can be categorized as follows:

- Debts from unpaid rent by tenants, which occur when tenants of the fund do not pay rent on time. This means that although the fund records income according to the lease agreement in its profit and loss statement, it does not receive actual cash (Cash) , resulting in the fund having to record assets from overdue rent debts or Accounts Receivable (A/R) , leading to a lack of cash and potentially preventing the fund from paying dividends as usual. If overdue rent is not paid in the future, the fund may incur additional expenses from allowance for doubtful accounts. Investors can review these details in the financial statements of the fund to see if the receivables from tenant debts have increased compared to previous financial periods.

- Debts arising from loans for investment, which typically occur when the fund invests in new assets and has obligations to pay interest and repay loans. The borrowing criteria for Property Funds and REITs are as follows:

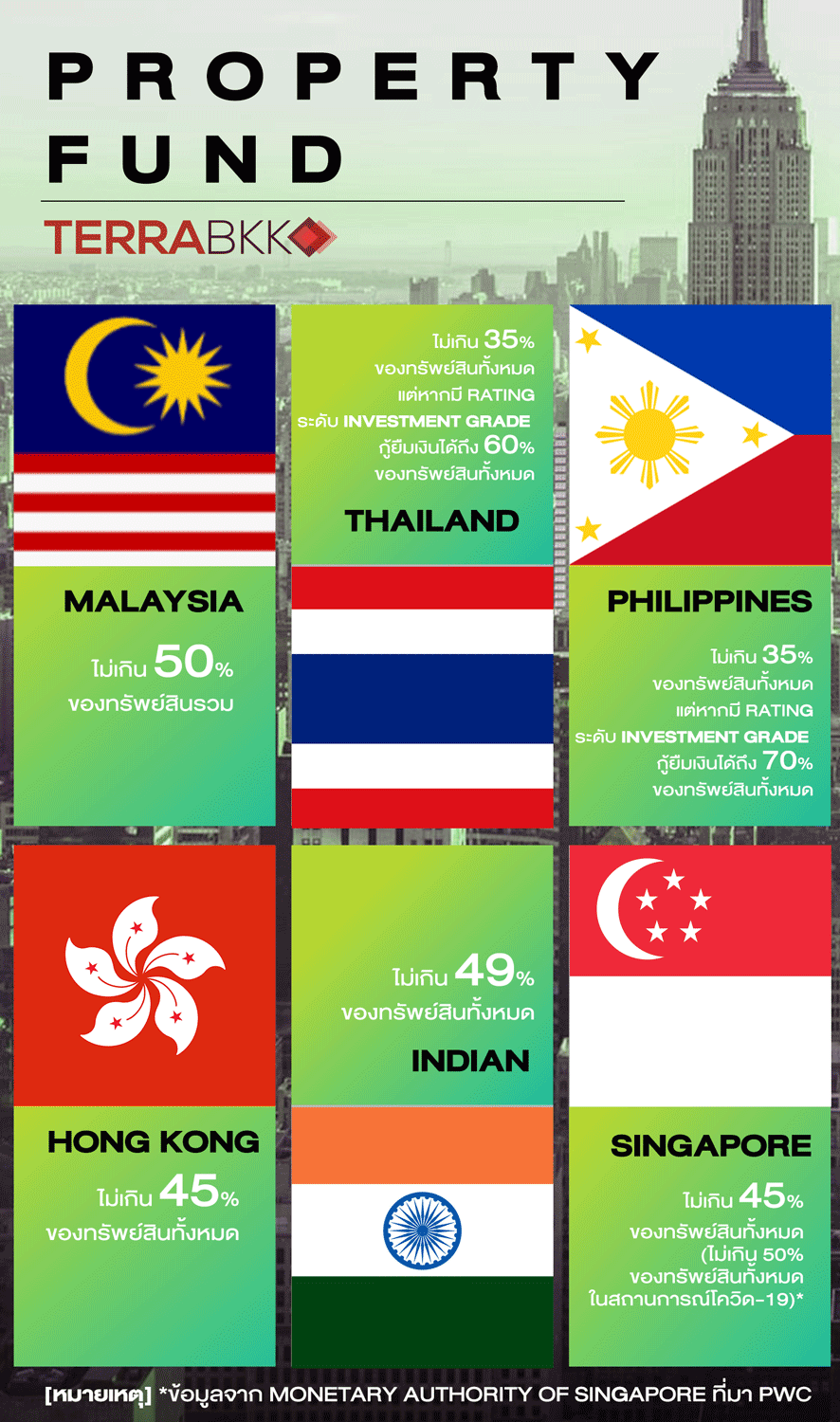

- Property Funds can borrow up to 10% of the net asset value (Net Asset Value: NAV).

- REITs can borrow up to 35% of total assets, and if they receive a credit rating at the investment grade , they can borrow up to 60% of total asset value (Total Asset Value: TAV).

The borrowing criteria for REITs in Thailand have a relatively low ceiling compared to the criteria of REITs in neighboring countries.

Borrowing criteria for REITs in various countries.

[Note] *Data from Monetary Authority of Singapore

Source: PWC

In the industry, it is found that there are only a few Thai Property Funds in the market that have borrowed money, such as CPNCG, POPF and TLGF, and they can borrow only a limited amount. Therefore, they face risks from high interest burdens from loans that are not substantial. Meanwhile, most REITs have some level of borrowing to reduce financial costs when acquiring assets, but this can be a double-edged sword if the REIT cannot meet interest payments during a crisis. Certainly, the fund must prioritize debt and interest repayments before considering profits available for dividends to unit holders.

However, the risk that REITs will be unable to pay interest is relatively limited, as these funds generally have a low level of borrowing. Currently, the average debt ratio of REITs in Thailand is about 24.3% of total asset value. Some funds have debt ratios exceeding 30.0% of total asset value, which is close to the borrowing limit of 35% of total assets, such as CPNREIT, BKER, HREIT, MIT, SHREIT and LHHOTEL. Some funds may have agreements to defer interest payments initially or negotiate debt repayment extensions with creditors, avoiding defaults. Investors should study the details of each fund further.